{kind=link}

The BIS once released a report on clearing houses on 31st October, 2022.

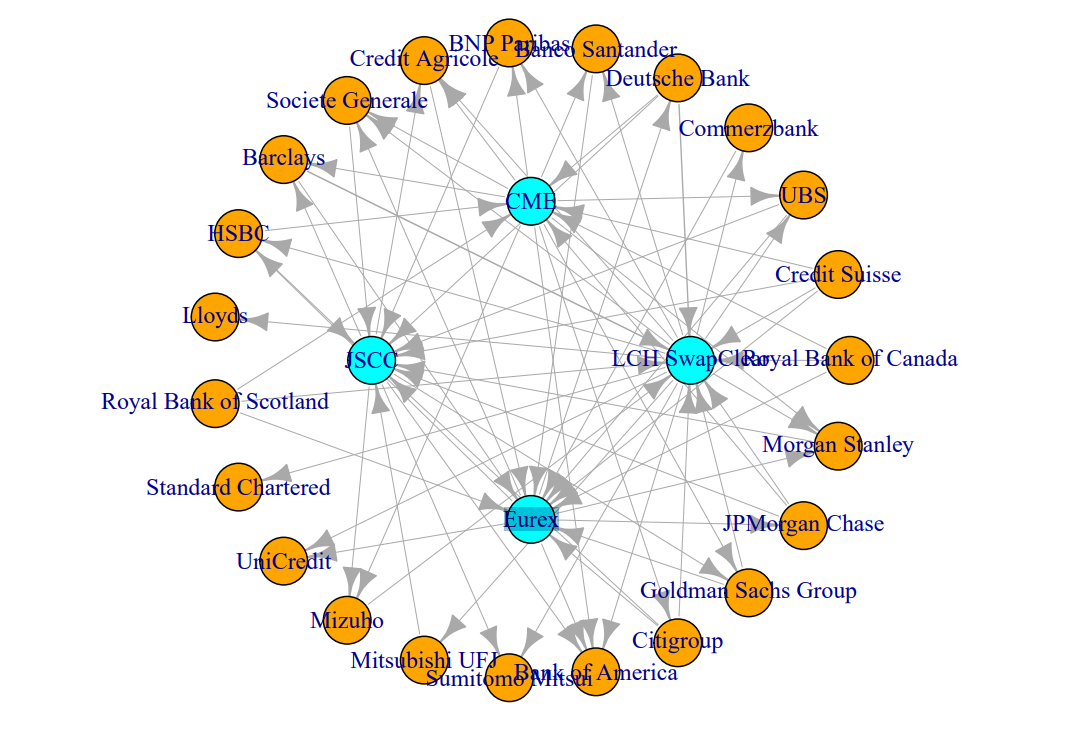

The report clearly pointed out that if Credit Suisse or Deutsche Bank collapsed based on the current scale of interest rate swap, there would be a funding gap of more than $9 trillion.

The current internationally accepted stress test for banks (Cover 2) actually does not take into account the "network effect" of the entire clearing system, which leads to the fact that the so-called "stress test" cannot truly reflect the real bearing capacity of the tested bank

The Credit Suisse crisis is the best example. It proved that when a market maker engaged in interest rate swap transactions fails, it will trigger the so-called "network effect" and cause the collapse of the entire clearing network. And Credit Suisse actually passed the so-called "stress test" at the beginning of this year.